You can identify if you are inside the Social Security Benefits Tax Torpedo by looking at two numbers from your Form 1040 individual federal income tax return. If you are inside it, it could be as high as a 40.7% effective federal marginal tax rate or, if you have any long-term capital gain or qualified dividend income, as high as 49.95%.

This means that if you took another $100 out of your IRA or 401(k), you would pay $50 more federal income tax. Is there anything you can do about if you are in the 40.7% or 49.95% effective marginal federal tax rate bracket? Yes.

Two taxable events are happening. First, you thought you were just taking money out of your traditional retirement account, but it leads to more Social Security benefits being taxed. That is why the effective marginal federal rates are so high, such as 49.95% if you have any qualified dividend or net long-term capital gain income. If you do not have either of these, the rate can be 40.7%.

The most Social Security benefits that anyone can have subject to tax is 85%. If you receive $10,000 in Social Security benefits, then $8,500 would be the maximum subject to tax or included in your income.

The numbers on your tax return can tell you whether you are inside the Social Security Tax Torpedo range. Look at your total Social Security benefits for the year and the amounts included in the income of those Social Security benefits. So, let us say Social Security benefits were $10,000, and let us say that the taxable amount is $7,000. Well, $7,000 divided by $10,000 is 70%. You are in the Tax Torpedo range.

Now, what if your Social Security benefits were $10,000 and the amount included in your income was $8,500? Again, that is the maximum possible. You have now gone through the Social Security Benefits Tax Torpedo, which has hit you, but your taxable income now puts you above it.

Keep in mind that if someone is married filing jointly and both spouses are collecting Social Security, that would show up as one tax return for Social Security. There are over 60 million tax returns that report Social Security on them. Two-thirds have none of their Social Security benefits included in income or are taxable; they are below the Social Security Tax Torpedo. However, 10 million returns out of 60,000,000, or 1/6th, have some of their Social Security benefits taxable but below 85%; they are inside the Tax Torpedo. There are 10 million others with 85% of their Social Security benefits included in their income or taxable. They are above the top of the Social Security Tax Torpedo; they went through it. They had some of their income taxed at these significantly higher rates.

Where exactly is the worst part of the Social Security Tax Torpedo? It is different if you are single versus married filing jointly. If you are single for 2022, once your taxable income goes above $41,775, you jump from the 12% federal marginal tax rate to 22%. When do the 40.7% and 49.95% rates happen? They happen when the taxpayer’s taxable income increases from 12% to the 22% federal marginal tax bracket. Once you jump into the 22% effective federal tax rate bracket, your additional income is taxed at either 40.7% or, if you have any qualified dividend or long-term capital gain income, 49.95%.

To demonstrate the effect of this 40.7% marginal rate, say someone was single, at the top of the 12% bracket, and they decide, “Oh, I need a little more spending money.” So, they take out $1,000 more from their tax-deferred retirement account. You might think, “Well, he went from the 12% to the 22% bracket. So, on that $1,000 of additional income, they should pay another $220 in tax.” They do not. They pay $407 more tax. Why? When they took $1,000 from their tax-deferred retirement account, another $850 of Social Security became income or taxable.

So, you now have $1,850 more in taxable income because you took $1,000 more out of your tax-deferred retirement account. The additional $407 in federal income tax is a marginal rate of 40.7%.

But remember, we all get deductions. If nothing else, we get the standard deduction. The standard deduction for a single person aged 65 or over is about $15,000 in both 2022 and 2023. That is why when total income gets above $57,000 if single and above $112,000 if you are married filing jointly, and if you are collecting Social Security, you will get into the worst part of the Tax Torpedo. For 2023, this total income will be closer to $120,000 for married couples, and there will be a $30,000 standard deduction.

What Can You Do to Avoid the Social Security Tax Torpedo?

So, what can you do? If you plan your taxable income such that you will get to the top of the 12% bracket (which again is a 22.2% effective federal marginal rate) and you are collecting Social Security, do not take any more money out of your tax-deferred retirement accounts, your IRAs, your 401(k)s. If you need more cash for the year, take it somewhere that does not trigger income. If you have any Roth IRA money, take it from there or draw from a taxable savings account.

Another suggestion: if you have yet to start Social Security, if you are in good health, if you have other sources for spending, then delay Social Security. You will get hit by the Social Security Tax Torpedo in fewer years. The fewer years you get hit by the Social Security Tax Torpedo, the better, purely from a tax efficiency standpoint and a lesser amount of the present value of federal income taxes you will pay over the years. Delaying Social Security is consistent with being more tax efficient. If the person lives a long life, there will be significantly fewer taxes than if they started Social Security earlier and were in the worst part of the Social Security Tax Torpedo most every year.

Other options are to

- Sell stocks where there is less appreciation

- Take a distribution from a Roth

- Take funds needed from an interest-bearing taxable account, or

- Take it out of a stock where you will have a capital loss or a little capital gain.

All these things can help you avoid the worst part of the Social Security Tax Torpedo.

The only way to do this is to figure out where you are as the year progresses. It is too late at the end of the year. Granted, once you turn age 73, you have required minimum distributions from all your IRAs and 401(k)s and other tax-deferred traditional retirement accounts. Social Security has started by the time you are 70, and many people, in this case, cannot avoid the worst part of the Social Security Tax Torpedo high effective marginal federal tax rates. In many cases, you could have done some things before you turned 70. Whether you started Social Security before age 70, keep your income to the top of the 12% bracket in taxable income.

How to Avoid Additional Medicare Premiums (IRMAA)

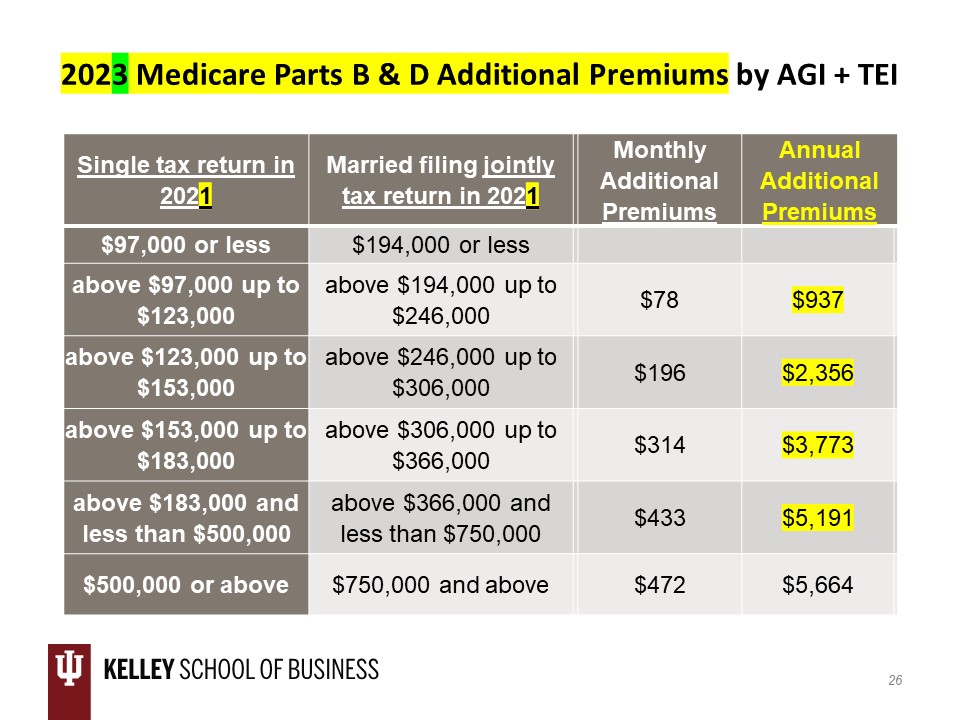

IRMAA stands for Income Related Monthly Adjustment Amounts. These are adjustments that increase how much Medicare premium you must pay. 2023’s additional Medicare premiums are based on your 2021 adjusted gross income (AGI) plus your tax-exempt income. If anyone has to pay additional Medicare premiums in 2023, then two income amounts on their 2021 tax return exceeded the threshold.

Can you do anything to reduce or avoid the IRMAA tax? Yes, you can. But keep in mind, if you do something to keep your income at a level in 2023 where you do not go into a higher IRMAA tax threshold, that will help you in 2025 because 2025’s additional Medicare premiums are based on 2023’s income tax return.

If you retire and it is determined that you have to pay additional Medicare premiums for the next two years, file Form SSA-44. It is not a federal tax return but a form you file with the Social Security Administration, not the IRS, asking them to use income from a more recent year for determining your Medicare premiums. You will tell them, “Do not use income from when I was working full-time, and I had all that salary income. Use income from a more recent year when I am retired and for figuring out how much additional Medicare premiums I must pay.”

On your 2021 tax return, if you are single and that amount is above $97,000, you will have to pay an extra $937 in Medicare premiums. What if you jump above $123,000 on your 2021 tax return in your income plus tax-exempt interest income? You are going to have to pay an additional $2,356 in 2023.

For those filing married joint, most of the amounts are double what they are for single. It is not taxable income; it is total income before any deductions. Most individuals’ adjusted gross income, if they are retired, is the same as their total income. But remember to add tax-exempt interest. In other words, municipal bond interest, state and local government bond interest, they make you add that in.

Suppose you are married and filing jointly, and your 2021 adjusted gross income plus any tax-exempt immunity bond interest income is not over $194,000. In that case, you pay the regular Medicare premiums. Once you get one dollar above $194,000 on your 2021 tax return for total income, you must pay $937 more in Medicare premiums.

What if both spouses are on Medicare? They would pay $937 for one spouse and $937 for the other, or almost $1,900 in additional Medicare premiums. Part B of Medicare is commonly called “medical.” Part D is commonly called “prescription drug.” Both of those premiums can increase if your total income gets above the threshold of $194,000.

I call additional Medicare premiums a tax. Why? Because it is based on two numbers off your tax return, adjusted gross income plus tax-exempt Muni interest. So, investing in Muni bonds does not solve your problem if you are high-income and must pay additional Medicare premiums.

Filing SSA-44 to Lower Medicare Premiums

You can only file the SSA-44 if there is a life-changing event. Once during a different presentation, I was asked 25 different ways, “My income was high this year, and then it will be lower next year. Can I file the SSA-44?” No. Not unless it is a life-changing event, which includes significant work reduction or work stoppage, which includes retirement. Let’s say you sold a stock or a business and had a considerable income jump just for one year. That is not a life-changing event. You will be stuck with higher Medicare premiums two years later for that one year you had an abnormally high income.

You can file this SSA-44, explain that the work stoppage or the significant work reduction was your life-changing event, and use a more recent year’s lower income instead of paying the higher amount of additional Medicare premiums. You might reduce it down to no additional Medicare premiums.

Let’s say one spouse has already retired, and the higher-earner spouse retires at the end of 2022. Instead of having this couple reporting income for Medicare above $246,000 up to $306,000, they can report a more recent year’s income as not above $194,000. The spouse with the life-changing event can help the other spouse qualify for lower premiums.

You need to file an SSA-44 for each spouse because additional Medicare premiums are per person on Medicare. In other words, one spouse’s life-changing event, stopping work or significant reduction in work, can be the other spouse’s life-changing event that qualifies them for lower Medicare premiums too. If the second spouse doesn’t file an SSA-44, they could pay additional Medicare premiums of $2,356 per spouse or $4,700.

If your total income is one dollar above the income threshold for IRMAA, you will pay a lot more in Medicare premiums.

In other words, if you are single and your income in 2021 is $97,001, you must pay $937 more in annual Medicare premiums. What about going over $123,000, even by only a penny? You will pay $2,356 more in Medicare premiums because you exceeded the $123,000 income threshold. See how harsh the additional Medicare premiums you must pay are when you jump to a higher step?

How to Manage Medicare Premiums After the First Two Years of Retirement

So, what can you do? You want an income plan to keep total income from jumping into a higher threshold. That way, you will save on paying too much additional Medicare premiums two years later. How do you do this income planning each year? You want to make tax-efficient decumulation, distributions, withdrawals, sales, spend-down, or whatever you want. You want to be tax-efficient in retirement, taking money out of your different accounts, such as taxable investments versus traditional retirement accounts versus Roth retirement accounts.

You want to be tax-efficient, with income going near the top but underneath the next threshold. How can you keep it from jumping to the next threshold if you need more income? Here is the conventional wisdom for tax-efficient decumulation/withdrawals.

- First, decumulate (i.e., “draw-down” or “spend-down) all investments held outside retirement accounts (i.e., “nonqualified”).

- Then decumulate all tax-deferred retirement accounts (e.g., 401(k)s, 403(b)s, 457s, Thrift Savings, IRAs—i.e., “Traditional”).

If you follow the above order, once the 2nd step is reached, $2,356 of IRMAA tax will be paid annually.

However, if subject to IRMAA, a taxpayer who gives to charity can reduce AGI and avoid paying $2,356 extra tax every year by making a Qualified Charitable Distributions (QCDs) (after age 70½) from IRAs:

- The distributions must go directly from IRA to the qualifying charity.

- These always reduce AGI.

- Non-QCD contributions to charity are itemized deductions that do not reduce AGI.

- For those who are at least aged 72, QCDs count toward an IRA owner’s required minimum distribution (RMD) for the year.

Be aware that investing in a taxable account can disrupt your annual planning. If IRMAA is an issue for a taxpayer, that is a good reason not to have taxable money invested in actively managed mutual funds because

- They have uncertain capital gain distributions annually, and

- That can trigger IRMAA even if you do good annual planning.

Suppose you have any money in a Roth account; that is one way to receive additional funds that don’t push your income into the next IRMAA threshold. Another way is to take funds from a qualified Health Savings Account that can be distributed if you have qualified medical expenses.

You can also take money from taxable accounts with a significant basis by selling some stock. Let’s say you have $60,000 of stock with a $37,000 basis or a $23,000 gain. You have $60,000 in additional cash flow but will only include $23,000 in taxable income.