How do you take all the different solutions and construct retirement income solutions that might work for you and your clients? The solution is to apply modern portfolio theory to the payout phase. Modern portfolio theory talks about asset classes and their different characteristics, the asset allocation decision, accumulating assets, and minimizing risks of investment losses. If we apply this thinking to the payout phase, now we’ll be talking about retirement income classes. The decision we’re focusing in on is the retirement income allocation decision. We’ll be looking at the amount of retirement income that might be generated and a lot of the techniques might look at the risk of income losses.

The retirement income generators available today are:

- Shared solutions, i.e. annuities

- Investing solutions

- Solutions that can be embedded inside a DC plan

- Solutions that could be implemented outside a DC plan, say through IRAs.

You want to understand the different features and pros and cons of different retirement income generators because they are all different:

- Different in the amount of income that they generate, both at retirement and throughout retirement

- Their guarantees are different

- Accessibility of assets are different, and

- There is not a one size fits all solution.

So it’s up to either plan sponsors or advisors for understanding the different characteristics of these different retirement income generators so that they can help their constituents.

In general, there are three types of retirement income generators and this applies whether it’s inside a defined contribution plan or in an IRA or other retirement savings.

- The first one is to invest your savings. You keep the principal intact and you just spend the investment income.

- The second is a systematic withdrawal program where you’re still investing your savings, but you’re withdrawing principal cautiously to avoid outliving the principal, but we’ll point that there’s no guarantee if you live a long time or if you have poor returns, there’s no guarantee that you might outlive your principal.

- The third RIG, or retirement income generator, is purchasing an annuity from an insurance company.

So we know that there are a lot of variations of each approach. The other thing we want to note is that the first two retirement income generators, whether you’re investing and taking out just investment income or you’re withdrawing principal cautiously, if you’re within a deductible IRA or a defined contribution plan, eventually you’re going to have the IRS required minimum distribution rules kick in at age 70½ and they might actually require you eventually to withdraw more money than your strategy might warrant under the first two retirement income generators.

Criteria for Plan Sponsors to Consider When Adding Income Solutions to Plans

So here a possible criteria that a plan sponsor might want to think about when evaluating different retirement income generators:

- What is the amount of retirement income that it’s generated?

- Do you get a lifetime guarantee or not?

- Do you have protection of the income in the period leading up to retirement?

- Do you have protection of potential for increases after retirement for keeping up with inflation?

- Do you have protection post-retirement or if there’s a stock market crash, will the income go down?

- Do you have access to funds?

- Do you have the potential for inheriting unused funds?

- Who’s controlling the investments and the withdrawal? Is that the plan sponsor through the retirement income program or the participant’s controlling the investments and the withdrawal amounts?

In this study we looked at six different retirement income generators.

- Systematic withdrawal plan using a constant four percent rule, where withdrawing a constant four percent of initial assets and then adjusted for inflation after retirement

- Four percent withdrawal of remaining assets

- A systematic withdrawal program using the IRS’ required minimum distribution

- An inflation adjusted SPIA

- A fixed SPIA

- A GLWB or GMWB annuity.

Our assumptions regarding future investment returns, both for stocks and bonds and cash, reflected the current low interest environment, both in our expectations for future bond returns, but also for current annuity purchase rates.

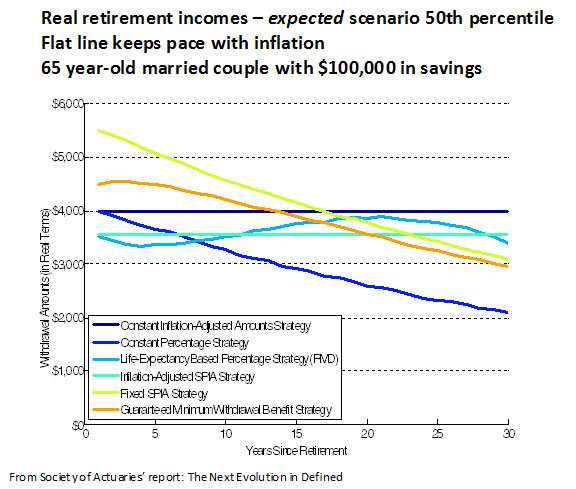

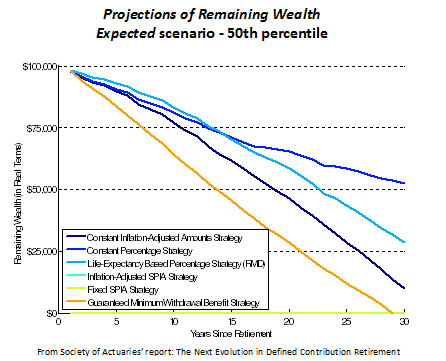

This first graph shows for someone who has $100,000 in savings, what is the expected amount of income that they might receive over their life? So each line represents a retirement income generator.

For a 65 year old married couple starting off with $100,000 in savings the income amounts are adjusted for inflation, so a flat line keeps pace with inflation. Each of these are viable retirement income generators, and they all have different patterns of retirement income. The fixed SPIA (lime green line) starts with the highest amount of retirement income but, because it’s fixed, it declines over time due to inflation in real amounts.

The flat line that you’re seeing is a constant. There are two flat lines. One is the four percent rule, which is always withdrawing amounts that are adjusted for inflation, and then the turquoise flat line is the inflation adjusted SPIA. Then you’ll see the other retirement income generators have just different patterns of how their income plays out over a 30 year period. One last point on this slide is this is what we call the expected scenario. So this is the 50th percentile of the stochastic forecast. So this is what we would expect, given our assumptions.

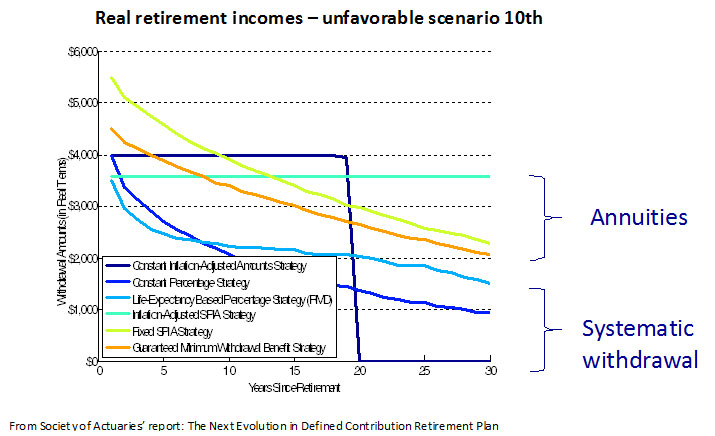

But now let’s look at what happens to real retirement income under unfavorable scenarios. At the 10th percentile of stochastic forecast annuities tend to do better than systematic withdrawal. Basically what we’re doing is we’re demonstrating with sophisticated analyses what we probably all know is that if the stock market does poorly, you really want to be in some kind of a product that is protecting yourself against stock market decline.

The most dramatic result here with systematic withdrawals is this blue line. That’s the four percent rule, where you’re just withdrawing four percent of your beginning assets, adjusted for inflation, and you’re ignoring what happens with your assets after retirement. If you just keep blindly withdrawing four percent, under a poor scenario, you’ll run out of money according to our forecast. At around 20 years, the fixed four percent rule exhausts your assets. This was the unfavorable scenario.

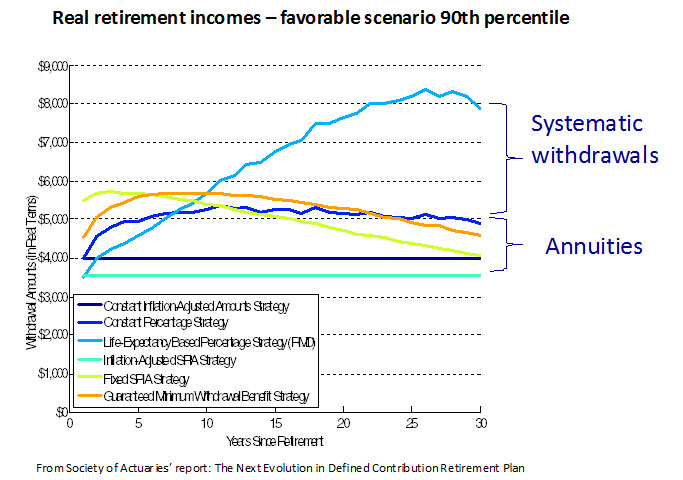

Under the favorable scenario, we looked at the 90th percentile and demonstrate that if the stock market does well, you want to be in a systematic withdrawal program and actually invested assets will produce more income than most annuity programs.

In sum, if the stock market does well, you’re better off investing your money rather than buying an annuity. The purpose of buying an annuity is to protect yourself against stock market decline and against long lives. These graphs just show the amount of income that you might get over a 30 year retirement.

Another analysis people might be interested in is remaining wealth. In this case, the retiree started off with $100,000 in savings. The flat line at the bottom is the SPIA, because once you submit your money to an insurance company and buy a SPIA, then you have no more accessible wealth.

The systematic withdrawal schemes and the GLWB annuity do have remaining wealth at different points in time. The GMWB annuity has the lowest amount of remaining wealth because there are fees being withdrawn from the assets to pay for the longevity protection. This is where GMWBs are a hybrid between a systematic withdrawal scheme that gives you complete flexibility and an annuity which gives you lifetime guarantee. GMWB gives you the best of both worlds, but then you’re having the lower amount of accessible wealth throughout retirement, compared to the other systematic withdrawal schemes.

If you withdraw at a faster rate with the systematic withdrawal schemes you’ll have a lower amount of accessible wealth over retirement. Conversely, if you withdraw at a very conservative rate, you’ll have more wealth over your retirement.

So putting it all together, retirement income strategies that we think make sense is to combine systematic withdrawal plans with annuities. Cover your nondiscretionary, basic living expenses like the roof over your head, utilities, food, and medical insurance premiums, by sources that are guaranteed to last for the rest of your life and won’t go down if the stock market crashes. Sources of that would be Social Security, pensions if you have one, and annuities.

Then cover discretionary living expenses; travel, gifts, spoiling your grandchildren with a systematic withdrawal strategy. What our analyses shows is if you’ve covered your basic living expenses with the guaranteed sources, then you can justify either a higher withdrawal rate or a more aggressive asset allocation with the systematic withdrawal strategy. Basically what we’re saying is that annuities, Social Security, and pensions become the “bond” part of your retirement income portfolio and then the systematic withdrawal retirement income generator is the equity or the stock part of your retirement income portfolio.

One last point we want to make at the bottom here is that the best systematic withdrawal solutions do adjust the retirement income to reflect emerging investment experience. That’s really resulting from that graph we saw where under unfavorable scenarios, if you just keep blindly withdrawing the same amount of money under a fixed four percent withdrawal strategy, eventually you could run out of money. We think that the best solutions actually will adjust the retirement income to reflect, whether you’re getting gains or losses, you’ll apply some formula to your remaining assets each year.

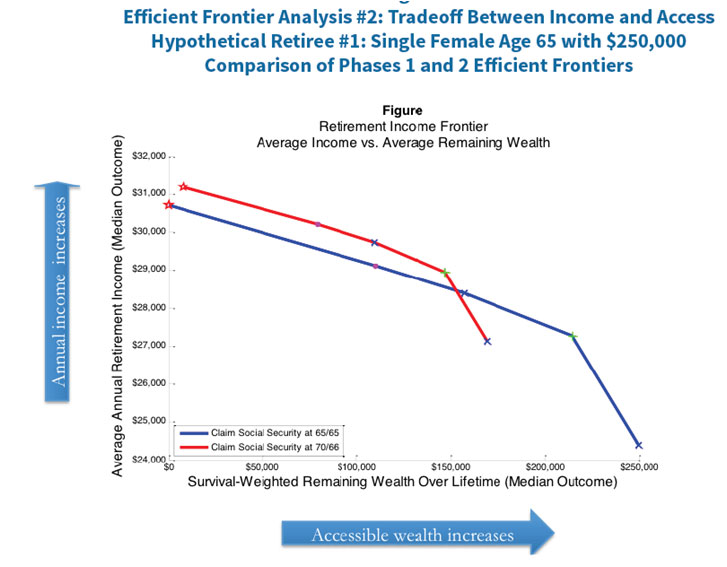

Balancing Expected Retirement Income and Accessible Wealth

Efficient Frontier #2 of the study analyzed balancing two goals: expected retirement income, and the ability to access wealth throughout retirement. We think for a lot of retirees, they may actually be focusing in on this efficient frontier instead of the first one.

So with this particular efficient frontier, the measure of return on the vertical axis, the Y axis, is the average amount of retirement income over the retirement period. The horizontal axis, the X axis, is the average amount of accessible wealth throughout the retirement time, adjusted for inflation and adjusted for the probability of survival to each age.

What about taking a portion of your savings to enable delaying Social Security? We assume that you retired at 65, but that the primary wage earner would delay taking Social Security to age 70 and withdraw from their savings between age 65 and 70 to make up for the Social Security benefit that’s being delayed. Then they would take their remaining savings and implement some kind of a retirement income solution with the remaining savings. We found that this strategy can increase expected total retirement incomes by amounts ranging from five percent to 12 percent, and the increase in the retirement savings was highest for solutions that had significant fixed income investments.

The increase in the benefit for delaying Social Security is more than an actuarial increase, so you can take advantage of that by delaying your Social Security benefit. You’ve got to invest almost 100 percent in stocks to have any hope of beating a delayed Social Security strategy. This is a significant concept that people should understand because if you’re willing to commit some of your savings to guaranteed solutions, you should start with delaying Social Security.

The chart above shows compares the efficient frontiers. The red line is the efficient frontier if you’d use this delay strategy. The blue line was the efficient frontier that shows the tradeoff between amount of income and liquidity. We do note here though, over to the right, the red line crosses the blue line. What this is saying is that if you do use your savings to delay Social Security, you are depleting that portion of your savings at a fairly fast rate.

So if you’re absolutely most focused on accessible wealth over your lifetime, that’s one scenario where you may not want to use a delay strategy. If you’re really, really focused on having the maximum amount of accessible wealth over your lifetime and you want to be down at that lower right hand corner, then you’ll probably not want to use your savings in the early part of your retirement to delay Social Security.

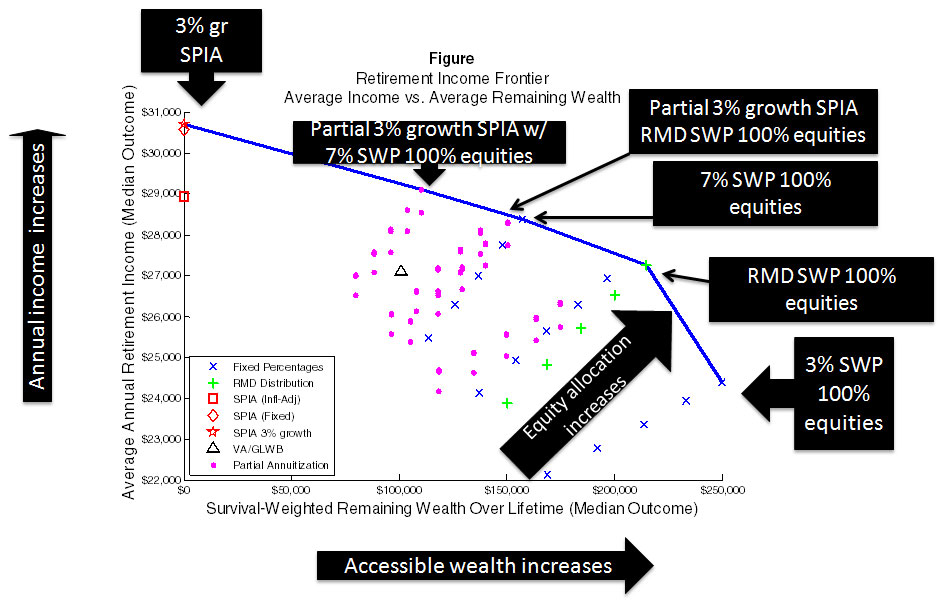

Determining an Acceptable Tradeoff between Expected Income and Liquidity

The rationale for this particular analysis is that people might be hesitant to devote substantial resources to irrevocable annuities so they can have access to those savings, either throughout retirement or to leave a legacy for unused funds. So what’s the acceptable tradeoff between expected amount of income and liquidity?

The vertical axis above is the average amount of retirement income from the solution. Each dot here represents a particular retirement income solution. The horizontal access is the average amount of remaining wealth over the lifetime of the retiree. So the efficient frontier here is the blue line that is, for any given point on the horizontal axis, the highest point on the vertical axis.

Now we can actually show different extremes. On the far left hand corner we see that the three percent growth SPIA produces the highest amount of income, but there is no accessible wealth. Nevertheless, it’s the highest vertical point on that horizontal axis. If you go all the way to the right on the bottom, you’ll see a three percent systematic withdrawal. We’re taking three percent of assets each year and investing 100 percent in equities. That produces the highest amount of accessible wealth we would expect, but then it also produces a low amount of average retirement income.

If you go along the blue line, you’ll see other points that are either on the efficient frontier or close to it. For example, just above the three percent systematic withdrawal plan is a required minimum distribution systematic withdrawal plan approach (green pluses) with 100 percent in equities. This approach provides more income compared to a three percent systematic withdrawal plan, but there’s a little bit less accessible wealth because you’re drawing down your assets at a faster rate.

The upper right most green cross is 100 percent in equities; from there the allocation to stocks decreases. The next green cross is 75 percent in equities; the next green cross is 50 percent in equities; then 25 percent; and then zero in equities. As you increase the allocation of the stocks, you get closer to the efficient frontier. What this says is if you’re doing a systematic withdrawal plan, this particular analysis recommends that you invest 100 percent in equities. We acknowledge that people won’t be comfortable with possibly, but this is what the analysis is showing.

At the second to the left most point, we see a three percent growth SPIA with a seven percent systematic withdrawal plan that can provide a three percent income bump every year. Thirty percent of the savings are devoted to the SPIA and 70% of savings were devoted to a seven percent systematic withdrawal scheme to create a retirement income solution on the efficient frontier. What we’re saying is you’ve got a diversified portfolio. You’ve got the bond part of your retirement income portfolio consisting of a SPIA and Social Security. A seven percent SWP becomes the stock part of your portfolio, the retirement income portfolio, and if you invest that particular portion of your retirement savings in 100 percent equities, you’ll get the highest point on the efficient frontier.

Just because a particular solution is on the efficient frontier, that doesn’t mean it’s necessarily the best solution for a plan participant because there can be behavioral issues that can influence people wanting to take some solutions that may not lie on an efficient frontier, particularly if people are really worried about the risk of losing money, they may feel uncomfortable with a solution that has a fair amount of equity exposure even though our analyses demonstrate that that might be considered optimal.

Optimal solutions might combine investing retirement income generators with insured generators like annuities, and they’ll also integrate with Social Security claiming strategies.