The Exit Planning Institute studied business owners and asked them if they felt that a transition strategy was important for their future and their business. Ninety-nine percent of them agreed with that statement. However, 79 percent of owners had no written plan, 48 percent had yet to do any planning, and many had not thought about what they would do next. They also looked at the most trusted advisers in their transition teams. CPAs were the most trusted advisers, followed by Corporate Attorneys and the business owners’ spouses. There’s a real opportunity to work with these advisers to accomplish an effective business sale.

Business owners have often been mentored, which makes them more generous. Fidelity did a study, and they found that entrepreneurs gave 50 percent more than non-entrepreneurs when they gave to charity. Also, when they volunteered, they volunteered two or more hours per week than non-entrepreneurs.

All this creates a wonderful opportunity for those in the financial tax legal field to help business owners create what they want for the next phase of their life, their retirement. One thing to consider with business owners is that they are not like dogs – they do not want to be told what to do even if they’re paying for advice – they are more like cats. If you want to advise business owners, think of them like cats and let them think that they are the ones generating the ideas and that you are there to support them.

Tax-Advantaged Business Sales and Other Assets

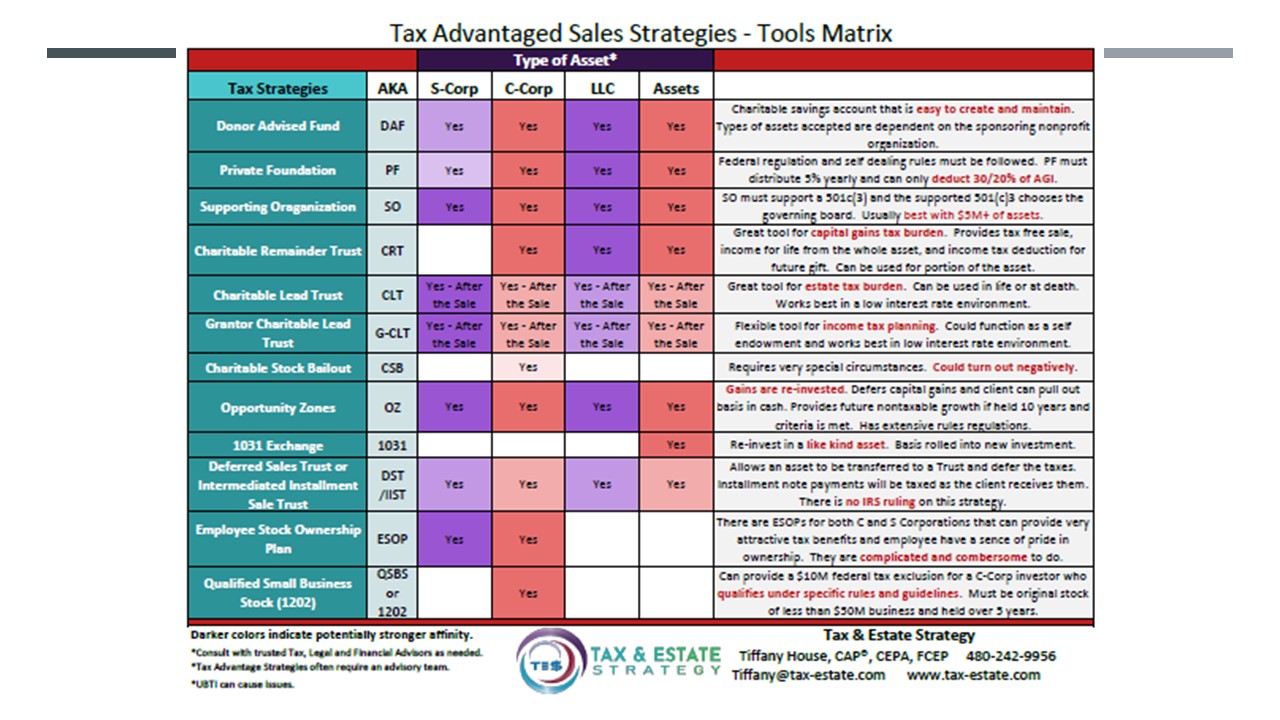

Below is a cheat sheet I created for tax-advantaged business sales.

On the left side of this chart are different tax strategies, most of which we will cover in this article. The next column over is AKA, or “Also Known As .” Then we have S-Corp, C-Corp, LLC, and assets.

I try to make it simple to understand what type of tools you can use in certain situations with different business structures. Some of the boxes are darker than others, meaning it’s a little more relevant or easy to accomplish. If it’s a lighter color, it might not be the strategy that I would go to first, or you might have to ensure that it is appropriately structured by someone who knows what they’re doing, particularly with S-Corp stock.

Let’s go into the structure of businesses. Seventy-three percent of all businesses which file with the IRS file as an S-Corp. An S-Corp is a pass-through entity for tax purposes, meaning that the owner of the S-Corp will pay taxes at their personal rate for anything that comes through the S-Corp. One thing to consider with S-Corporations is the unrelated business taxable income or UBTI, which can get in the way of some charitable planning tools and other planning tools.

If a charitable remainder trust has UBTI associated with it, it will be taxed at 100 percent. So, we do not put any UBTI assets, unrelated business taxable income assets, inside a charitable remainder trust. But we can use other tools like a supporting organization or a Donor-Advised fund.

C-Corps are taxed at a corporate level, and when the proceeds are paid out to the owners, they are taxed at their personal level. So, C-Corporation income is double-taxed.

LLCs (limited liability corporations) can choose how they are taxed; they can be taxed like an S-Corp, a C-Corp, or a disregarded entity if there’s only one owner in the LLC.

Assets like land and buildings are taxed at capital gains tax rates and have a lower depreciation recapture rate of only 25 percent. Other assets can go up to your ordinary income tax rate. This is important to know when we’re dealing with a sale of a business because sometimes it’s going to be a stock sale, and sometimes it’s going to be an asset sale.

Partnerships are also pass-through entities, but each partnership has different governing documents. If you’re dealing with a partnership, you must go back to the governing documents and look at how it is structured inside the document to see what kind of planning strategies you can utilize. That is why you did not see Partnerships on my cheat sheet because you can only state clearly once you read each document.

Regarding stock sales versus asset sales: One thing that is looked over often by 75% of business owners is if they own an S-Corp, they think they can sell the stock, and they think it will be sold at capital gain taxes. Business owners and advisers must realize that buyers don’t want to buy S-Corp stock. There are a few reasons; one is that a liability could still be attached to the business before the change of ownership. If you buy the stock of an S-Corporation and an employee feels they were wrongfully terminated, they could come back and sue the new owners. Or there could be a problem with vendors or customers as well.

Another reason buyers don’t want to buy S-Corp stock is because they can get a step-up in basis by buying the assets instead. Many business owners are utilizing a 15-year depreciation schedule, and some are even doing accelerated depreciation on some of the assets within the business. If a buyer bought the stock, they would have to assume the same depreciation schedule. However, if they bought the S-Corp’s assets, they could get a step-up of basis, which would benefit them for tax purposes.

Donor Advised Funds

Now we’ll dive into the meat of this topic. We’re going to go through some of the strategies on my cheat sheet, and I’ll share with you some of the case studies that I worked on where this was a pertinent planning strategy tool.

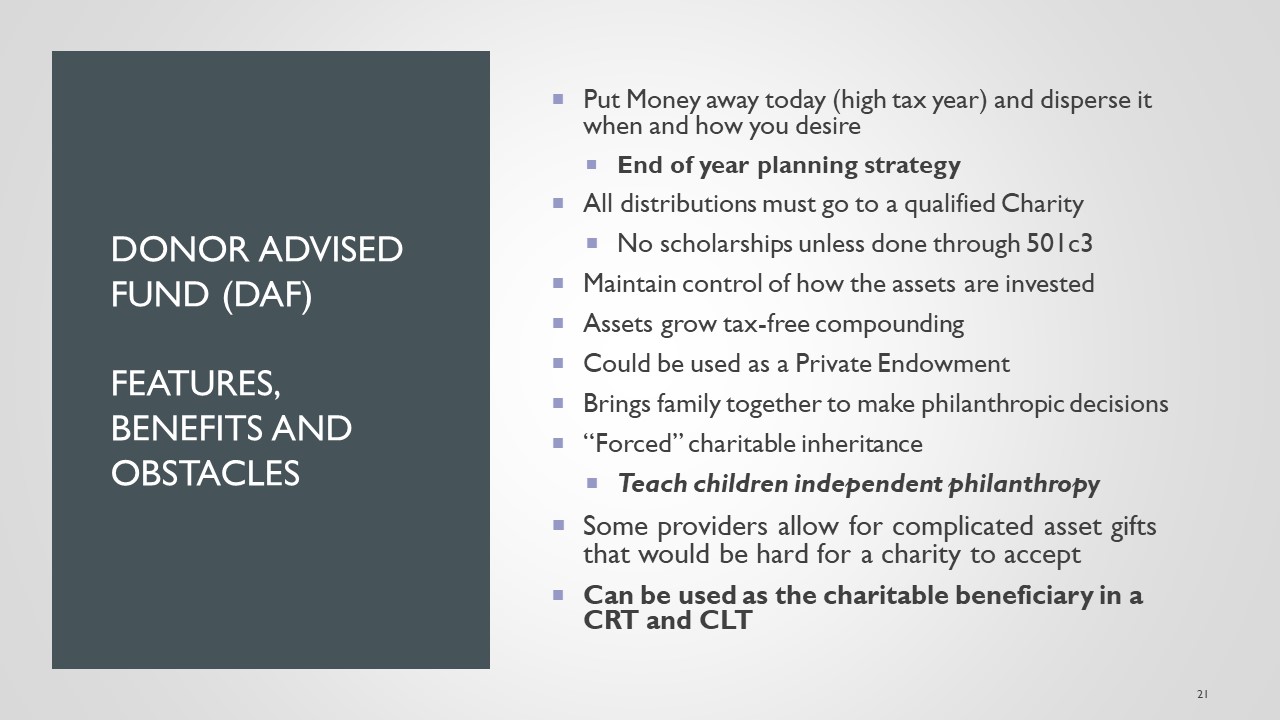

A Donor-Advised fund is like a private charitable account where a person can set aside their charitable savings account and get the tax benefits upfront. It’s taxed a lot like an outright gift to charity because, essentially, the Donor-Advised fund is a 501(c)(3). One of my favorite things about a Donor-Advised fund is that it’s a great way to teach philanthropy to future generations.

Who is an ideal candidate for a Donor-Advised fund? It’s usually someone who

- needs an immediate income tax deduction

- intends to leave a legacy

- has considered forming a family foundation

- is a high-income earner

- wants to include the family in charitable planning

- wants to give to multiple organizations and simplify the accounting, and

- desires anonymity in their giving.

You’ll also see sometimes that people will bunch their gifts in one year utilizing a Donor-Advised fund. But it can be an excellent tool for anybody who is listed here as an ideal candidate, and they only have to have one of the attributes below.

I had a client who owned an insurance company with his father. The father was ready to sell, and a large national insurance company thought they were perfect for acquiring. It worked out well that the majority of the sale of this business, which was an S-Corp, was personal goodwill. This is great because personal goodwill is taxed at capital gains tax rates, whereas corporate goodwill is taxed at ordinary income tax rates.

We already had a good structure for how the business would be sold. However, this gentleman had had a bit of a rough go earlier in life where he had fallen onto a destructive path, so now he gave 10 percent of his income to charity. He necessarily wasn’t religious; he didn’t go to church, but every time he received a check for anything, he gave away 10 percent. So, we went ahead and did a Donor-Advised fund for him at the time of the sale so that he could get a big tax deduction upfront and then be able to fund his future charitable endeavors.

It all starts with choosing a sponsoring 501(c)(3). Fidelity Charity, Raymond James Charity, and other broker-dealers have put together their own Donor-Advised fund program. There are also the Community Foundation or other large nonprofits, and private organizations like the American Endowment or Charitable Solutions that have Donor-Advised programs. The type of asset being sold is how I choose who will the sponsoring 501(c)(3) for the Donor-Advised fund.

So, the donor gets to make their own little fund inside the sponsoring organization. They make that gift and get that tax deduction right up front. The nice thing about this, particularly with this gentleman and his father with the insurance company, is that he wrote checks to charities every month because he was constantly giving away 10 percent. His accountant now loves me because only one receipt needs to be provided, and that’s the gift he made to the Donor-Advised funds. As the Donor-Advised fund pays out to charity at different time frames whenever the donor decides, there’s no reporting necessary because they received the tax deduction upfront.

One of the other opportunities I like with Donor-Advised funds is to use them as an end of your planning strategy, as some people have a last-minute, “Oh shoot, I have a big tax liability coming up .” They can get that deduction this year and put their gifting into future years.

It is also a great way to teach children philanthropy. My husband and I have a Donor-Advised fund, and we ask our kids to grant from it twice a year. They have to research the charities. If you have any clients with children concerned about the direction their lives are heading, a Donor-Advised fund is a great way to help them guide future generations into the direction they might find more suitable for them.

Finally, one of my favorite things about a Donor-Advised fund because it can be used in conjunction with other charitable planning tools, and it can be the charitable beneficiary of the charitable remainder trust and a charitable lead trust.

Supporting Organizations

A Supporting Organization (SO) is a mix between a private foundation and its Donor-Advised fund. It has to support a 501(c)(3) organization or a class of 501(c)(3) organizations. A Supporting Organization is an excellent tool for complicated assets. An ideal candidate for a Supporting Organization is someone who is thinking of selling their business and wants higher adjusted gross income limits for gifting than they would be able to get from a private foundation. They want to maintain some control and don’t want to pay capital gains taxes on the assets.

A woman I work with is in business with her two brothers; they specialize in alternative investments. They have a unique portfolio and will be selling four or five of their businesses worth about half a billion here within the next five years. The first asset we’re working on is bouncy houses, and their warehouses are full of trampolines, blow-up things, and what-have-you that generate great cash flow. They are looking to sell this asset and then move into other businesses.

The sister wants to give to a charity that helps homeless people. She wants to buy bulk mattresses and donate them to an organization because she does not think the charity will manage the money properly or get a good deal on the mattresses. I spoke with her about putting one of their complicated assets into a Supporting Organization. Now she can designate a class of charity – it doesn’t have to be one charity – of 501(c)(3) organizations. She could donate to charities that the local Community Foundation. You can make it very broad as to what 501(c)(3) you can support. My suggestion to her was to create the Supporting Organization with the LLC interest in one of the buildings inside the Supporting Organization. Then, she can liquidate them inside the tax-exempt entity and save taxes.

Supporting Organizations have received a bad name in the past. There are three types of Supporting Organizations, and Type III was overly used. The Pension Protection Act cracked down on it, and now Type III Supporting Organizations have similar rules to that of a private foundation and are much more scrutinized. However, Type I and II are not scrutinized and have higher adjusted gross income limits, meaning that you can give more each year to the Supporting Organization. It provides a great opportunity for complex assets like S-Corp stock.

A Supporting Organization is a great tool for complex assets; however, I usually only look at it when there are over $5 million. Other tools could be utilized instead, like a Donor-Advised fund or sometimes a Family Foundation.

Charitable Trusts

One of my favorite tools is Charitable Trusts. There are three kinds of Charitable Trusts, all of which have been in the tax code since 1969. The three types of Charitable Trusts apply to different tax problems.

- The Charitable Remainder Trust is what I look to for capital gains tax issues. It can also help with income, estate taxes, and other taxes, including state taxes. But if you hear of capital gains taxes, your Charitable Remainder Trust is the go-to tool.

- If there’s an income tax issue, a Grantor-Charitable Lead Trust is the tool I suggest looking at first or with other tools that aren’t charitable.

- A Charitable Lead Trust or Non-Grantor Charitable Trust is a perfect tool for an estate tax issue. It’s fabulous, and you can wipe out all estate taxes. It’s easy to do, and as I mentioned, it’s been in the tax code since 1969.

So, I see Charitable Trusts as the Swiss Army knife of planning. You do not have to have a charitable client necessarily to talk about some of these charitable trusts. In those cases, I’ll call them Tax-exempt Trusts. I have talked to plenty of people who were not charitably minded or did not want to give their money to a charity; instead, they wanted to give it to their kids. I showed them some of the tax benefits and how they would end up with more by giving some.

Charitable Remainder Trust

The Charitable Remainder Trust (CRT) is for capital gains taxes, net investment income tax, state tax issues, and depreciation recapture can all be solved within a Charitable Remainder Trust. It needs to be more utilized by most.

Let’s pretend we have an apple tree, and with this apple tree, we can take the asset, the apple tree, and put it into a Charitable Remainder Trust. The donors can act as trustees, fertilize it, grow it how they want and have a say over how the investments are managed. They’re also able to get the apples or the income for life which makes them quite happy. At the end of life or end of term of years, their tree will be then transitioned over to a charity, and that provides some great tax benefits. The donor can get lifetime income, they get an income tax deduction upfront for their future gift of the tree, they get to save taxes now, and they get to nurture the tree as trustees.

An ideal candidate has a highly appreciated asset and accompanying capital gain on which they’re concerned about paying capital gain taxes. They can also be considering selling a business, own rental properties, perhaps not charitably inclined, and would like to convert to a ROTH IRA or other tax-related concerns.

I have used a CRT very successfully with a ROTH IRA conversion for an IRA that was quite significant. We were able to do a Charitable Trust at the same time and utilize the tax deduction upfront for the ROTH conversion so that this client could convert to a ROTH without having to pay any of the taxes.

A couple from Minnesota had a plastics company. Minnesota has a very high-income tax rate state. They were ready for retirement and selling their C-Corp for $18 million. They wanted to ensure their son was cared for because he had been very influential in the business. He was a great employee, and they wanted to make sure that he received things from the sale. We set up trusts to be able to get assets outside of the estate and utilize the estate tax exemption. Their son (and a daughter) were given stock that was put into the trust so that assets could grow inside their trusts. Their kids ended up with a good majority of the business, and they were quite happy at the time of the sale.

Then we put $5 million also into a Charitable Remainder Trust from which this couple could get income for life. They were very charitable, so they were excited about supporting their charities in the future. The tax savings was the kicker to help them decide to do a Charitable Remainder Trust.

As an example, we’re going to look at the sale of a $2 million-dollar business just for the simplicity of numbers. I rarely put 100 percent of an asset into a planning strategy, such as with the plastics company, where we utilized some of their estate tax exemption and gave assets to their kids, which grew over time before they sold it. We also did a Charitable Remainder Trust for only $5 million because we wanted to make sure that we utilized the deduction the best we could while allowing them to keep money outside these planning tools.

With this example, we will split the $2 million-dollar business sale in half, and we’re only going to put one million dollars into a Charitable Remainder Trust. We’ll allocate half of the business interest – this is a business that has no tax basis as the founder started it – and we’ll title that and put it into a Charitable Remainder Trust. When we do this, there are no taxes, which allows us – in this example – $288,000 in tax savings. Where did I get that number? The federal capital gains tax rate is 20 percent, we have the 3.8% Medicare or net investment income tax, and an estimated 5 percent state tax, totaling 28.8 percent. If they put half of their business into the Charitable Remainder Trust, they save $288,000.

Upon the death of the second donor, the funds left over benefit charity, or it could also fund their own Donor-Advised fund. They can navigate it from the grave and leave their kids in charge of the Donor-Advised fund, instructing them to have a family meeting once a year to determine who will get funds from the Donor-Advised fund.

Because of their future gift to the charity or the Donor-Advised fund, this 65-year-old couple could get a $275,000 income tax deduction upfront, which greatly benefited them. They wanted to take a six percent income from the trust, so the first year’s distribution was $60,000 – this was a unitrust, so the income did fluctuate – but if they lived their joint life expectancy of 30 years, they would have received $2 million of income.

What if leaving something to the kids is your client’s most important objective in their planning? You can buy a $1 million life insurance policy and supplement or replace the asset. For example, you can make ten years of payments of $30,000, so $300,000, and we’ll take that out of the income paid to the donors, which makes their lifetime income $1.7 million after the life insurance premiums. The kids still get one million dollars of inheritance, and the charity or Donor-Advised fund gets $1.3 million (the initial $1 million plus $300,000 in life insurance premiums).

But the neat thing is that income tax deduction of $275,000. If you had that taxed at a 40 percent income tax bracket, the owners are saving $110,000 that they could invest and use for the future. When you add up the capital gains tax savings of $288,000, that’s $398,000 of tax savings. These tax savings can then be utilized to sell the other portion of the business.

I will often do half of an asset or less; sometimes, it’s only for about 25 percent. It depends on the taxes that can be saved and which deductions can be utilized. So often, we do not determine how much is going into the CRT until we’ve talked to the client’s accountant, figured out their tax liability, and what we want to offset with that income tax deduction.

Another nice thing about this tool is if you can’t use it all the first year – the adjusted gross income limit for putting funds into a Charitable Remainder Trust is 30 percent – if you can’t utilize that deduction the first year you can use it in future years up to six (first year plus five). So, in this example, we were able to not gift $288,000 to the IRS but instead keep the assets growing tax-free inside the trust. This income tax deduction can be used this year or in future years, and it’s great for a ROTH IRA conversion. It also helps if you have estate tax issues; you pull that asset outside the estate for estate taxes, which can provide some asset protection.

We also need to compare this to what would happen if we did not use a trust. In this example, we’re only going to take half of the asset we put in the trust or $1 million of a business with no basis. We put those funds into an investment portfolio at the time of sale and pay the $288,000 tax to the IRS. We still take the same six percent annual income distribution to the owners, but now from a smaller asset, so they only receive $42,000 a year compared to $60,000 in our previous example. This reduces their lifetime income for the same life expectancy to about $1.25 million.

The kids will get an inheritance of around $850,000, which is less than our previous examples because there was less in the investment portfolio in the first place. Charity gets nothing, and the IRS is the big winner because there is no income tax deduction, and the capital gains tax is paid.

Let’s compare the sale of a business with no trust and the sale of a business utilizing a Charitable Remainder Trust. There can be $1.25 million without utilizing a trust or $1.7 million when utilizing a Charitable Remainder Trust, even after we paid life insurance premiums. The inheritance went from $850,000 with no CRT to $1 million with the CRT because of the life insurance purchased. Charity became the big winner as it was $0 with no CRT and $1.3 million with it. There are only income tax savings with utilizing a Charitable Trust. Still, the income tax savings for using the Charitable Trust, if you take the $275,000 deduction that we discussed earlier and tax it at about a 40 percent tax rate, means that they had $110,000 more in their pocket.

If we invest the $110,000 income tax saved over the same life expectancy of 30 years, that’s over $800,000. In sum, the total benefit of selling straight-out is $2.1 million to the family, but when we use a Charitable Remainder Trust, the total benefit is $4.8 million. You can say, “Okay, great, charity got $1.3 million of that.” However, when you look at it, the family still came out $1.5 million ahead on $1 million in assets by utilizing a Charitable Remainder Trust.

The only real threat with the Charitable Remainder Trust is if the donors don’t live to life expectancy. That is why you can also do a Charitable Remainder Trust with a term of years. Recent clients were selling a dermatology practice and said, “We don’t want to pay taxes; we give to charity, but that’s not our main motivation. We have two sons we like and one son we don’t. We want to go ahead and give income to two of the kids and leave the third son out.”

So, we did a Charitable Remainder Trust with them that included 20 years of income for the two sons they liked. That did make their income tax deduction less because less was going to charity, but they were less concerned about that. They wanted the income; they wanted their kids to receive income, and they did not want to pay taxes on that sale. So, the CRT was a great way to create a legacy and accomplish tax-free compounding growth.

Most Charitable Remainder Trusts can be invested just like a typical stock portfolio and other investments, which most financial advisers will also suggest. The assets inside the Charitable Trust are growing tax-free, so they can be utilized to accomplish more strategy versus a portfolio that isn’t inside the trust and, therefore, will be taxed whenever there are changes and diversification in that portfolio.

An important consideration is life expectancy. People who give to charity live longer than those who don’t. I have done over 30 charitable trusts, and no one has ever died short of their life expectancy; if anything, they live past their life expectancy.

Another important consideration is that a Charitable Remainder Trust works best in a high-interest rate environment. It uses something called the AFR 7520 rate. The rate for October 2022 was 4.0, November 2022 was 4.8, and December 2022 was 5.2. The higher the interest rate or the AFR rate, the more that deduction will be and the higher their deduction will be upfront for their gift.

The CRT is an excellent tool for real estate, raw land, publicly traded securities, closely held businesses, apartment complexes, and any asset that is highly appreciated. It’s preferable without debt, so you need to manage the debt before putting it into the Charitable Trust, but third-party nonprofits will help you with that. They will go ahead and manage the debt so that you can put the property or assets inside the trust.

Charitable Lead Trust

The Charitable Lead Trust (CLT) was made famous by Jackie Onassis Kennedy. With the Charitable Lead Trust, rather than giving the apples (income) back to the donor, we give the apples (income) to charity. Because we’re giving the income to charity, we can transfer the tree intact to the next generation. If we can do the CLT long enough, we can completely mitigate estate taxes.

The CLT is for any family

- concerned about estate taxes

- is charitably inclined

- cares about living a financial legacy to heirs and society, and

- wants to leave an inheritance to the next generation estate tax-free.

A CLT can be set up in life or at death. It is a great opportunity for those who know that they’re going to have to pay some estate taxes; to do the planning now and have it come about in the future.

For example, let’s say we have a $10 million asset. With a CLT, we are just putting a wrapper around the asset – like “Saran Wrap” – and then we’ll take income out.

The income of six percent a year is paid annually to charities or over $10 million over the 18 years of this trust. Because of this, we can zero out estate tax liability or create $4 million in estate tax savings. If the trust earns seven percent or eight percent, that $10 million can grow and come out entirely estate tax-free. It’s a great way to transfer assets to the next generation, and as I mentioned, it can be set up in life or death, but there are no adjusted gross income limits for it, so you do not have to worry about doing it in life.

Grantor Charitable Lead Trust

A Grantor Charitable Lead Trust (G-CLT) is the same concept but for clients with

- an income tax issue

- who are charitably inclined

- who care about leaving a financial legacy to heirs and society

- who need year-end tax planning, and

- who would like to convert to a ROTH IRA.

For example, a grantor puts $800,000 into a G-CLT trust (we put the same wrapper of the trust). We can determine the term of years (say a 10-year term), and they can get the $800,000 out at the end, plus or minus any growth. That allows them to give money to charities, say 5 percent a year for charity, so $400,000 will go into their Donor-Advised fund, which will give them an upfront income tax deduction for that future gift. So, the donor will get the $800,000 back after the term of years, but they got that large income tax deduction upfront for their giving.

That is a great tool to utilize for end-of-year tax planning when someone sold or did something, and they were not paying attention to the taxes and don’t want to pay the taxes, they can get that upfront deduction the year that they go ahead and do this. So in this example, the G-CLT provided a $175,000 tax break in the 45 percent tax bracket.

One thing to consider is that a donor still gets to be a trustee, so they have to say over how the assets are invested, but we have adjusted gross income limits here of 30 percent, and there is something called the phantom tax liability. Any growth inside the trust does have to be paid by the donor each year. So, something to consider when looking at that.

Here’s a quick difference between a G-CLT and a Non-Grantor style Trust. A G-CLT means the client will get the asset back; in both cases, the charity will get the income, and in a Non-Grantor trust, the kids will get the asset. So, in a G-CLT, the donor gets to keep the tree, gets the income tax deduction upfront, and is responsible for phantom taxes. On a Non-Grantor Trust or just straight-out for estate tax purposes, the donor gets to give the tree to heirs; they do not get an income tax deduction, they only avoid estate tax, and there are no adjusted gross income limits. There is also something called a Super CLAT that combines the two that can be a good tool for complicated situations.

Other Tax-Advantaged Business Sale Options

Opportunity Zones are awesome. They’re better than a 1031 exchange. The Tax Cuts and Jobs Act of 2017 created these zones across the country where people can only take the gains. That’s the beautiful part about an Opportunity Zone; you must take your gains and invest them into an Opportunity Zone. The Opportunity Zone must fulfill certain obligations by the government; it’s a little tricky, and there’s a lot to it. I recommend utilizing a third party who is making the investment, and your clients can then invest inside those already structured investments.

The client gets to defer taxes when they invest in Opportunity Zones, and they get to defer the capital gains until the tax year 2026, meaning they don’t have to pay it until 2027. They need to maintain the investment for ten years, and all growth over those ten years comes tax-free.

Key Takeaways

There are great opportunities for all involved with business sales. The thing to remember is that you need to start the conversation. You’re not on your own; it takes a team. Please utilize the cheat sheet as a guide for talking to your clients.

The tool that you utilize depends on how the business is structured. Remember that business owners are cats, not dogs, so don’t expect them to do what they’re told. Have them follow the laser pointer to where you want them to go. Remember that you’re not alone, and it’s not as complex as it seems.

This was a presentation that could change your perspective on Tax-Advantaged Business Sales. Here are some additional resources.

- Exit Planning Institute State of Owner Readiness Study: https://exit-planning-institute.org/state-of-owner-readiness/

- Fidelity Entrepreneurs as Philanthropists: https://www.fidelitycharitable.org/articles/key-insights-into-entrepreneurs-as-philanthropists.html

- Forbes Baby Boomers: https://www.forbes.com/sites/markhall/2022/01/25/unsexy-but-thriving-businesses-the-hidden-opportunity-gifted-to-us-by-baby-boomers/?sh=142aa70e4620

- JP Morgan $30 Trillion Opportunity: https://www.openinvest.com/articles-insights/how-to-prepare-for-the-great-wealth-transfer-to-millennials